2024 Year End Wrap Up

January 21, 2025

Little Competition Offers Advantage for Ready Sellers

March 3, 2025

Home Insurance Costs Steadily Rising

How much will rising insurance costs affect affordability?

Homeowners insurance used to be something of an afterthought when purchasing a home. Now, between expensive policies or the lack of coverage, it is playing a larger role in being able to close on a home.

My own policy has increased 79% since I purchased it in 2017. Granted, the replacement value of my home has increased in that period, but it is also a reflection of increased insurance outlays across the country, with LA fires potentially setting a record for costliest on record.

Mortgage lenders include insurance in housing expense ratio calculations when qualifying buyers; housing expenses consisting of Principal, Interest, Taxes and Insurance (PITI).

Increased insurance costs could start to have a meaningful impact on home affordability.

What models will insurance companies utilize to predict environmental risks?

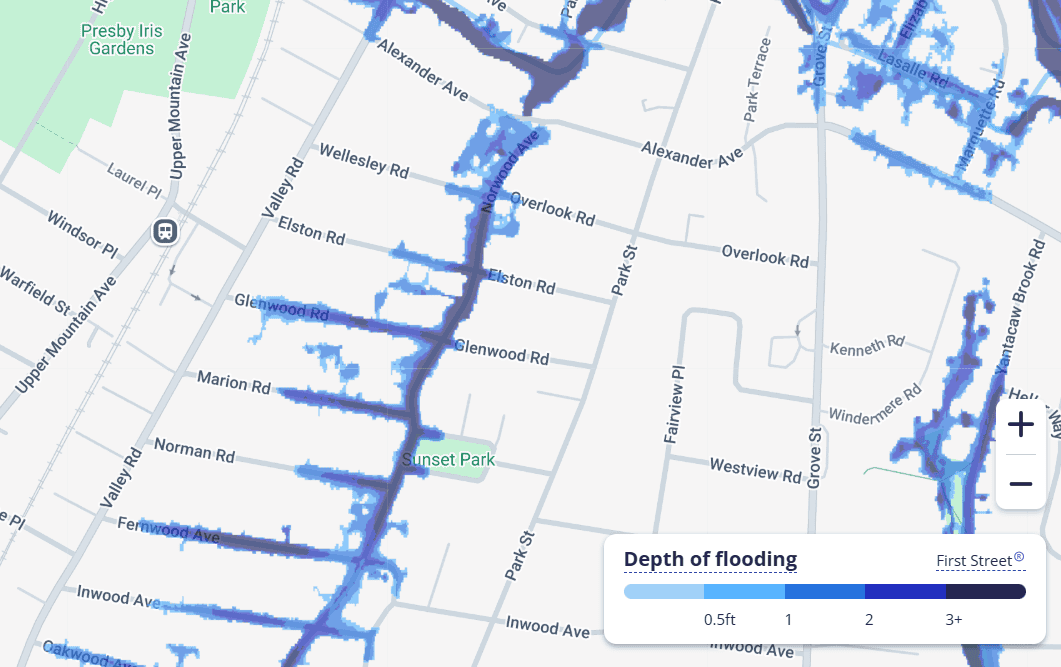

Well, if you scroll down on Zillow, you will note risk factors from a company called First Street. A potential buyer asked about a home we had listed being in a flood zone, and I was surprised since it was at least three quarters of a mile from an FEMA designation. They cited the Zillow designation.

I’m sure a lot of Upper Montclair residents would be surprised to see the risk of 3ft deep flood waters on their street (below).

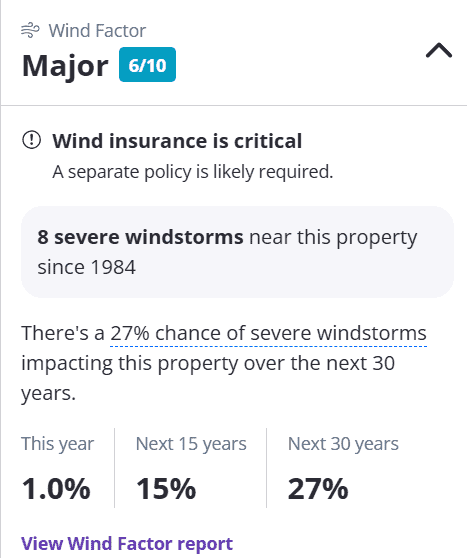

Also, most of Montclair is designated a high risk wind zone with wind coverage listed as critical. Most policies cover wind damage, but additional riders, deductibles and increased costs could be in the near future.

In summary, Insurance deserves to rank higher in your home buying concerns. Rely on your mortgage and insurance professionals to offer guidance.

Best, Rich

{kind=link}

{kind=link}

{kind=link}